Financial Fitness

Maria’s 2019 Goals:

- Get my financial world in order.

- See number 1.

What better time to address your financial health than with the approach of Tax Day, April 15th. This post is going to drier than the others, but hopefully, way more helpful. Consequently, it will be more financially rewarding for you.

Joy

The last 2 years have brought me much joy.

I blissfully finished up my employment contract with My Eye Doctor, which bought my practice, Unique Optique. After completing the selling contract of my favorite risk, I mentally moved on from both.

After renting out my house in Frederick, MD, I moved to be near my family in West Chester, PA. I rented an apartment for a year and then bought a house. The house came about as an unexpected blessing, one too Maria-perfect to pass up.

I went on a month-long, no-budget, no-holds-barred U.S. road trip with my dog. Having moved with my stuff but without a plan to make money, upon returning from the road trip, I had no job for 3 months.

After putting 50,000 miles on my car since moving, my much-loved but very worn Prius needed to be upgraded. I bought another hybrid.

For the first time in my life, I was an independent contractor. I needed to calculate and pay my own taxes on my income.

My financial world felt like I was standing in the middle of a cash grab chamber, goggles on, hair whipping around, grabbing onto the dollar bills that were suspended. Chaos.

I became obsessed with fixing the problem by soothing my uncertainty with knowledge. So, I listened to an endless number of podcasts, and read online articles. I called the companies where my investments were held, asked questions, and then called again when I had more questions. Then, I read books. Lastly, I scheduled interviews with many financial professionals, 7 to be exact.

Conclusion

While I am no financial expert, I thought that you might benefit from what I learned. Here goes.

Steps to financial clarity and freedom:

- Print out your credit report from all 3 major credit bureaus. Then pour yourself a glass of wine, read them thoroughly, and assure they are correct. Do this every year and correct any mistakes. Check your credit score. Do what you can to increase your credit score. (Time estimate 2 hours.)

- Get a credit card that gives you cash back and put all of your expenses on it. Pay it off in full every month. (If you aren’t financially able to do this, skip this step, as credit card fees are ridiculously high.) You can use the year-end reports to track where it all went. I researched credit cards and this is the one I chose for my general expenses. If you already have cards you like, call the company and ask for a lower interest rate, all fees waived, and a higher credit limit. Usually, they will give you all of the above. (Time estimate is 1 hour.)

- If you shop Whole Foods and Amazon, get this credit card. (Again, paying it off in full every month.) It gives you 5% off all of those purchases. (5 minutes)

- Use QuickBooks Self-Employed to track your income and expenses. With a simple swipe left or right, you categorize all money as personal or business. In addition, it also tracks your mileage via GPS using the same swiping system.

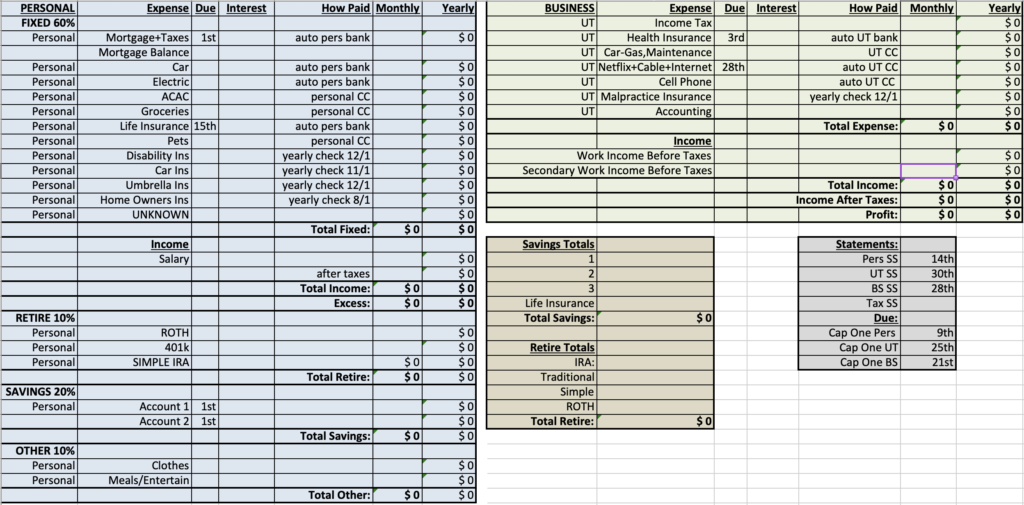

- Make a spreadsheet of all of your expenses and incomes. First, gather all the information about where your money comes from and where your money goes. Then, group these expenses into categories of fixed expenses (goal 60% of income), retirement (goal 10%), savings (goal 20%), and other (goal 10%). Mine is pictured and downloadable below. (The time estimate is 2-3 hours.)

- Use Personal Capital’s app and website to have all of your accounts in one place. They will graph and picture and maneuver and plan your financial picture efficiently and for free. (I considered using their advisors, but their fee is 0.89%, which is a bit high and will be discussed in number 13.) If you decide to join, use this link- you get $20 and I get $20. Personal Capital will also calculate your net worth. What should your net worth be? Here is an article that answers that question. (2 hours)

- Have 3-6 months of expenses in an easily accessible emergency fund. These expenses include basic rent/mortgage, food, insurances, car, gas, utilities, clothing, and entertainment. The best place to keep this money is a high-yield online bank account, of which CIT, Capital One 360, or Ally Bank are excellent choices. You will get around 2-2.5% return. (10 minutes)

- Figure out your best health insurance options. This may be simple if you are employed, or more complicated if you are an independent person with a lifelong, expensive diagnosis. I can only speak for myself, my disease, my state, and my finances. After months of researching and deliberating, I chose a high deductible plan with an HSA. You can deduct $3450 of that deductible from your taxes. You should put the amount of your deductible in an online bank account as discussed in number 7. (1/2 to 3000 hours)

- Write down your SMART goals, so you know where you are headed.

- Work towards paying off any high-interest loans on non-appreciating items. This means credit cards and car loans.

- Have a professional do your taxes. Usually, their knowledge and increased tax return more than pays their fee. If you are an independent contractor, know your tax rate so you know approximately what to put aside from each paycheck. Move that money into an online bank account and pay your quarterly taxes from that stash. If you are a business owner, have your accountant calculate your quarterly payments and print your payment slips. (3 hours to gather your tax information and 3 minutes to call the accountant)

- Invest whatever money is left in retirement IRAs first, then low fee, highly diverse index funds. Learn from Warren Buffett who made a 10-year wager with hedge fund managers that his basically-ignored index fund would outperform their constantly-adjusted expertise. Warren Buffett’s return on investment? 7.1%. The Hedge Fund Managers? 2.2%. Buffett FTW…

- Choose an expert with whom you should invest your money. This website lets you look up any financial person and tells you in which category they are. They are either “brokers” or “investment advisors”. Brokers may have a conflict of interest, as they get paid a commission from the products they sell. Investment advisors have a fiduciary duty to their client that requires them to put their clients’ interests ahead of their own. Registered investment advisors often earn a percentage of assets under management regardless of how many transactions a client does. Conflicts of interest could still be present when deciding between investing and doing something else with your money. There are two different compensation models for investment advisors: fee-based or fee-only. The difference is that fee-based advisors are paid directly by clients and they receive commissions from the products they sell. By contrast, fee-only advisers do not sell any financial products. They are incented, as a fiduciary, to search for the best options for you. They look for low fees, tax efficiency and are not required to use any particular brokerage house. Summary: To save on fees charged to you, find a fee-only fiduciary investment advisor to manage your money. If you have a financial person you love, sometimes relationships are more important than the fees. Just be informed. Do it yourself if you are smart enough. (I am not.) (2 hours)

- If you do it yourself, you could put your money into one fund and leave it, Warren Buffett style. There are 2 that work well for this manner of thinking, Vanguard VTSAX or VOO. Both have a 0.04% expense ratio. This way, the only fee you pay is the expense ratio.

- Consider robo-advisors. A robo-advisor is a diversified investment account that is automatically managed by a computer algorithm (as opposed to a human money manager). As the investor, you choose a goal and how much to invest. Then, the algorithm chooses the right asset allocation to get you there using a collection of low-cost mutual funds or exchange-traded funds (ETFs). The computers keep your portfolio balanced automatically over time and whenever you invest more money. For this service, the robo-advisors collect a modest fee averaging 0.30%. There are some hybrid models that also have access to a human advisor. Here is a link to a comparison chart where you enter what is important to you and it tells you which company is most compatible. I initially chose Betterment for their low fees, computer monitoring, constant rebalancing, ability to speak to a person, and tax loss harvesting. One further contemplation, I chose Vanguard because they have a stellar reputation in the financial world, are located nearby in Malvern, many of my friends work there, and their employees speak extremely highly of the company. (2 hours)

- Consider socially responsible funds. This philosophy rewards companies for good citizenship, as defined by ESG. The acronym stands for environmental, social and governance. Companies with high ESG scores are mindful of their environmental impact; treat employees, customers, and suppliers well; and have policies that align the interests of management and shareholders. Companies that stand out in these areas will be more successful over the long haul than companies that don’t. They tend to have above-average exposure to health and technology and below-average holdings in the industrial, materials and utility sectors.

- Don’t forget to donate to any charities that speak to you. Keep an eye on how much goes to the actual cause.

- Keep a spreadsheet or list of all financial websites, usernames, passwords, and account numbers for easy access to ALL of the money you have saved and ALL of the money you owe. (2 hours)

- Write a will. Either consult your attorney for help with this or if your estate is relatively simple, use Free Will. Or you can use Suze Orman for all of your most needed documents, including the below. (30 minutes)

- Write your Advanced Health Directives and Durable Power of Attorney for Healthcare. Here is a website that provides the download for the correct form for your state. (30 minutes)

- Create and fund a Revocable Living Trust for your assets with titles. This includes houses, cars, bank accounts and will save your beneficiaries a ton of money and time after your death.

- Consider or re-evaluate your life insurance. Do it for your loved ones.

- Reassess all of your insurances. Ask a professional for a quote for car, umbrella, disability, homeowners, etc. You may be surprised how much lower the payments can be.

- Take pictures of all of your important documents. All credit cards, front and back, driver’s license, registration for your car, financial responsibility card, insurance cards, AAA card, health insurance card, debit card, passport, marriage or divorce decrees, and birth certificate. I made folders in my phone photo album labeled “Wallet Cards”, “Car Cards”, “Documents”, etc. Mainly I did this out of laziness, and not wanting to get off the couch while online shopping and needing a credit card from my wallet. And in life, I often forget my wallet, but always have my phone. (30 minutes)

- Next, scan all important documents. Download CamScanner to your phone. Get a fireproof lockbox for your home ($30) or a safe deposit box at your bank. After scanning the documents (including number 18, 19, 20, 21, 22, and 23) tax returns, education documents, marriage/divorce certificates, advanced health directives, and will), save them in 2 different places- the iCloud, and your hard drive. Determine what computer filing system works best for you and organize the files so that you can be sure to find them again. Then, place the hard copies in a ziplock in your secured box. You will have a total of 4 copies of all your important documents, one picture on your phone, 2 saved digitally elsewhere, and 1 hard copy.

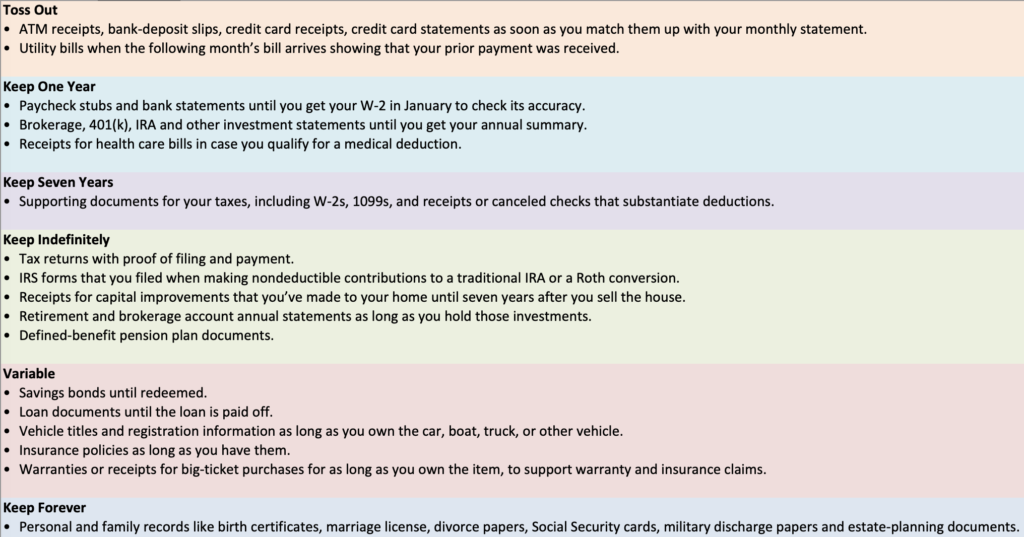

- Know when to throw away what. See the downloadable chart below for specific information. (2 hours)

- Discard any papers that you can get online. This includes bank and credit card statements, utility bills, health insurance EOBs. See below for a download of what to keep and for how long. (2 hours)

- Store any papers that you need to keep in Rubbermaid containers labeled with the year. That way, when the time period to keep has passed, you can go through and discard by year.

In Summary

You will feel so much better once you see how all of your financial pieces fit together. Be patient with yourself, take it one baby step at a time, and you will soon feel financially fit. In time, you will at least able to walk up the financial hill without huffing.

6 Comments

Kelly

Such an amazing and comprehensive guideline for financial sanity! Thank you for putting this together. I’ll be using it as my financial checklist 🙂

marhiggins

So glad you liked it! Hopefully it will save you some of the rabbit holes that I went down. Every turn I made, another rabbit hole. Hope it helps. Xoxo

Meg

This is fantastic! I will read this again when I have more time and follow your lead! Thanks for sharing all your hard work.

marhiggins

I am so glad you liked it. I hope it helps! I am still finishing up some of the points myself…

Whitney

This was so helpful! Thank you!

marhiggins

You bet!!